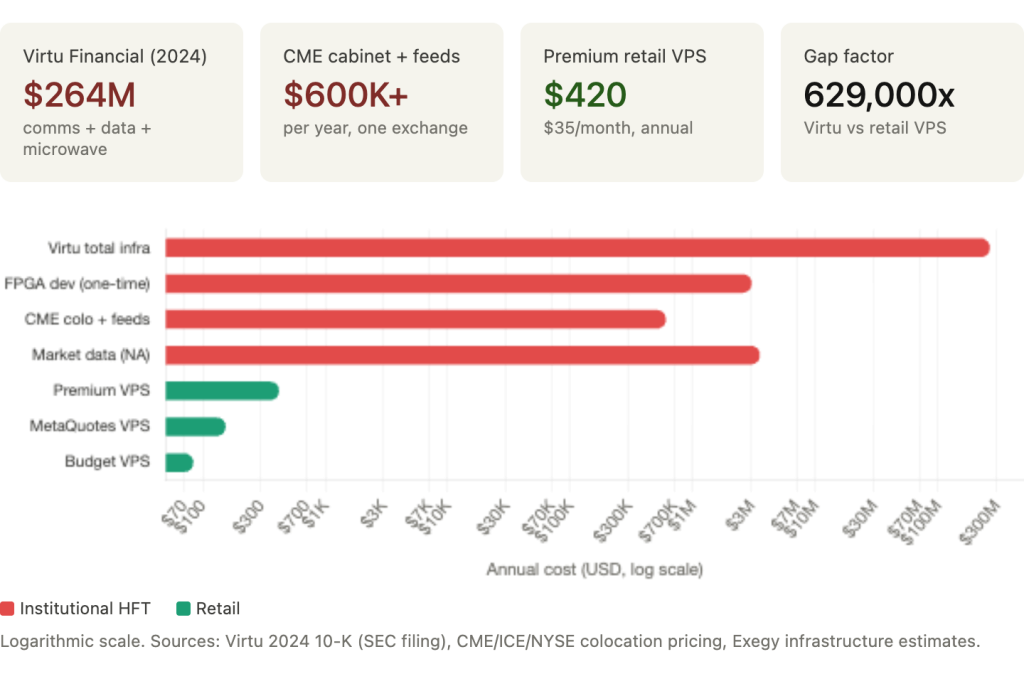

Virtu Financial, one of the few publicly traded high-frequency trading firms, reported $236.4 million in communication and data processing expenses for 2024, plus $27.7 million paid to microwave network joint ventures for the fastest possible New York-to-Chicago data transmission. Their trading servers run custom FPGA chips that process market data in nanoseconds, billionths of a second, inside exchange data centers where a single cabinet costs $15,000 to $19,000 per month.

A $35/month VPS running MetaTrader occupies an entirely different universe of trading technology.

This distinction matters because Forex VPS providers routinely market “HFT VPS” products to retail traders, creating a false equivalence between low-latency hosting and genuine high-frequency trading. The infrastructure, capital, regulatory, and technological requirements of real HFT are so far removed from retail trading that the comparison is not just misleading. It is physically impossible to bridge with a virtual private server running MetaTrader.

This article maps the exact gap with specific numbers: what regulators define as HFT, what the institutional tech stack costs and how fast it operates, where MetaTrader’s architecture creates hard ceilings that no VPS optimization can breach, and where the diminishing returns curve breaks for retail latency investment. The goal is not to discourage traders from buying a VPS. A well-placed VPS remains the single highest-ROI infrastructure investment for active retail algo traders. The goal is to redirect spending toward the speed improvements that actually produce measurable results, and away from marketing that promises something a retail platform cannot deliver.

Data is drawn from SEC and MiFID II regulatory definitions, IEEE-published FPGA latency measurements, exchange colocation pricing, MetaTrader execution benchmarks from MQL5 forums, the BIS Working Paper on latency arbitrage, the LMAX Transaction Cost Analysis study, and broker execution reports. Where a claim comes from a single source or a commercially interested party, it is flagged.

What Regulators Actually Mean by “High-Frequency Trading”

The term “high-frequency trading” has no single legal definition, which is part of why VPS providers can use it freely in marketing. But the regulatory descriptions that do exist immediately disqualify any retail setup.

The SEC’s 2010 Concept Release on Equity Market Structure identifies five characteristics of HFT: use of “extraordinarily high-speed and sophisticated computer programs” for generating, routing, and executing orders; use of colocation services and individual data feeds to minimize network latency; very short timeframes for establishing and liquidating positions; submission of numerous orders that are cancelled shortly after submission; and ending the trading day in as close to a flat position as possible. The Congressional Research Service explicitly notes that HFT remains “an imprecise catchall term that currently has no legal or regulatory definition” in the United States, but the SEC’s functional description makes the infrastructure requirements clear. None of these characteristics describe a MetaTrader terminal on a VPS.

Europe’s MiFID II provides the most concrete quantitative thresholds. Article 4(1)(40) defines high-frequency algorithmic trading as requiring infrastructure “intended to minimise network and other types of latencies,” including colocation or proximity hosting, combined with system-determined order initiation, generation, routing, or execution without human intervention, and high message intraday rates. Commission Delegated Regulation 2017/565 quantifies “high message rates” as at least 2 messages per second per instrument or 4 messages per second across all instruments. This sounds achievable until you consider the critical regulatory requirement that accompanies it: MiFID II requires anyone using HFT techniques to be authorized as an investment firm. Not a retail trader running an Expert Advisor.

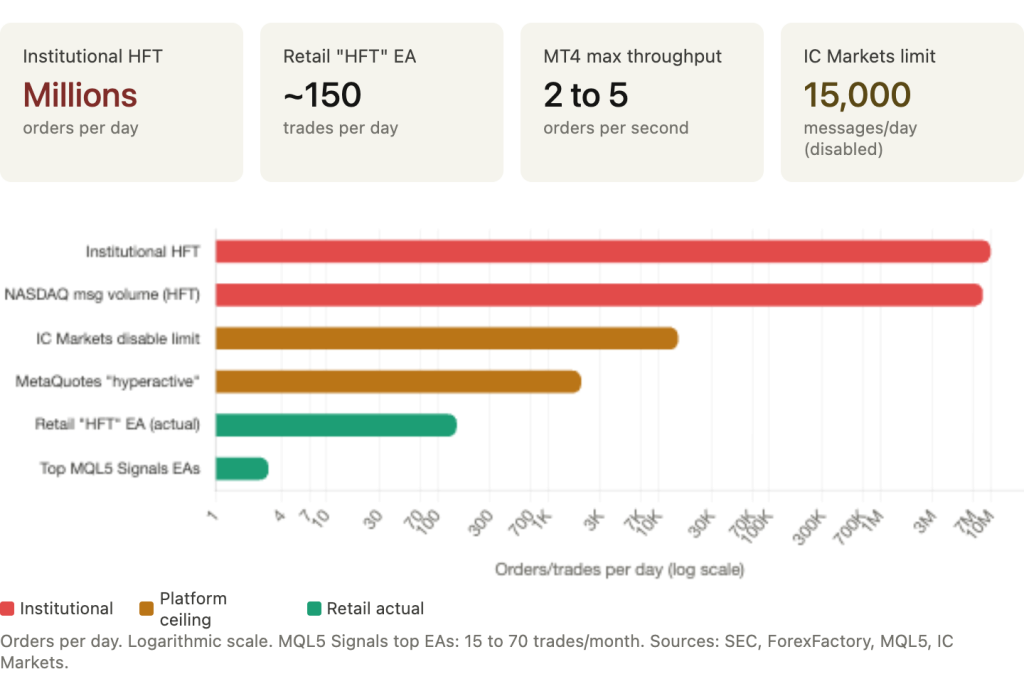

The order-to-trade ratios reveal the operational reality that separates HFT from everything else. SEC data from NASDAQ shows classified HFT firms had average order-to-trade ratios of 11.2 to 1 and higher, meaning for every trade that actually executes, 11 orders are submitted and cancelled. These firms represented 32% of dollar volume on NASDAQ but generated 94% of all order messages. Academic research finds approximately 96% of trading orders on US equity exchanges are cancelled, with roughly 40% cancelled within 500 milliseconds of submission. HFT contributes more than 80% of limit order messages on exchanges like NASDAQ-OMX Stockholm.

This volume and velocity of message traffic is architecturally impossible on MetaTrader. The platform was not designed for it. MetaQuotes considers accounts exceeding 2,000 server messages per day “hyperactive.” IC Markets issues warnings at 3,000 messages per day and forcefully disables accounts at 15,000 messages per day. The practical maximum throughput on MT4 is approximately 2 to 5 orders per second. On MT5, perhaps 5 to 15 orders per second. Real HFT firms submit thousands of orders per second on a single instrument. The gap is not a matter of optimization. It is a difference in what the software was built to do.

The Real HFT Tech Stack Costs Millions and Operates in Nanoseconds

True HFT infrastructure bears no resemblance to a Windows VPS running MetaTrader. The hardware alone reveals the gulf.

FPGA chips, Field-Programmable Gate Arrays from Xilinx/AMD or Intel/Altera, cost $20,000 to $80,000 each. They process market data directly in hardware logic, bypassing the operating system entirely. There is no Windows. There is no software layer interpreting instructions. The trading algorithm is burned into the chip’s physical circuitry. Custom FPGA firmware development runs $1 to $5 million over 6 to 18 months of engineering. The most aggressive firms go further: custom ASICs (Application-Specific Integrated Circuits) cost roughly $30 million per fabrication run and are designed to do one thing, execute a specific trading strategy, faster than any general-purpose hardware can.

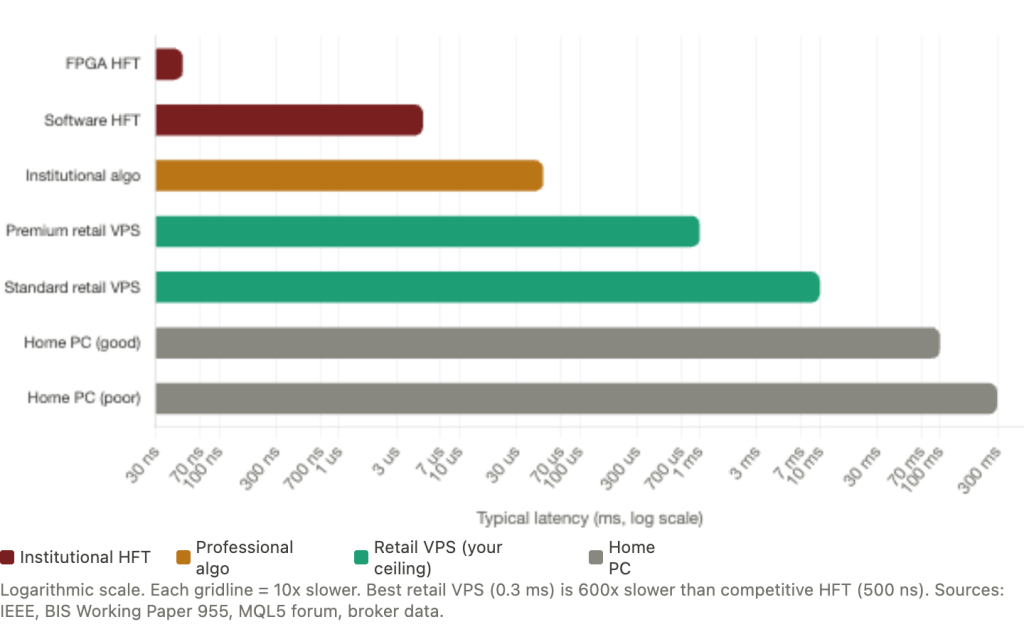

The latency figures operate in units that retail traders never encounter. Current top-tier FPGA systems achieve tick-to-trade latency in single-digit to double-digit nanoseconds, billionths of a second. A documented IEEE paper measured FPGA average latency at 480 nanoseconds. Optimized software systems using kernel bypass networking (Solarflare OpenOnload or DPDK, which eliminate Linux kernel overhead from the network path) operate at 1 to 10 microseconds. Standard optimized software without kernel bypass runs at 10 to 50 microseconds. Every one of these figures is measured in units that are invisible to a MetaTrader terminal. MT4 OrderSend() operates in hundreds of milliseconds. The gap between 480 nanoseconds and 480 milliseconds is a factor of one million.

Colocation is non-negotiable for HFT. Trading servers sit physically inside exchange data centers, not in a data center near the exchange, but inside the same building, sometimes the same room, connected to the matching engine by dedicated fiber measured in meters. Mahwah, New Jersey houses NYSE. Carteret, New Jersey hosts NASDAQ. Aurora, Illinois serves CME. Equinix LD4 in Slough handles London markets. Cabinet rental at CME’s Aurora facility runs approximately $15,500 to $19,000 per month. ICE Chicago colocation ranges from $3,300/month for a basic 3kW cabinet to $12,000/month for 10kW. Cross-connects, the direct fiber links to matching engines, add $500 to $15,500/month each depending on port speed. A single 10-gigabit LCN port pair at NYSE costs $15,500/month. This is the cost of a single cable connection to one exchange.

Market data feeds represent another expense category that has no retail equivalent. Premium direct exchange feeds cost $5,000 to $50,000+ per month per feed. OPRA, the US options data feed, alone requires 40 to 100 Gbps of networking infrastructure to process. Exegy estimates that building in-house market data infrastructure for full North American coverage costs $4.74 million, with $3.5+ million per year to maintain. Virtu Financial’s $236.4 million annual communication expense and $27.7 million in microwave network payments provide the most concrete public benchmark for what competitive HFT infrastructure actually costs.

The software stack runs exclusively on custom C++ (or increasingly Rust for safety-critical components), Verilog and VHDL for FPGA firmware, and proprietary binary protocols like SBE, ITCH, and OUCH for exchange communication. Not MetaTrader. Not MQL. Not Windows. The entire software environment is purpose-built for a single objective: minimizing the time between receiving a market data update and having a response order acknowledged by the exchange.

MetaTrader’s Architecture Makes HFT Physically Impossible

MetaTrader 4 and MT5 were designed as retail trading terminals, not execution engines. Their technical limitations create hard floors that no amount of VPS optimization, no hardware upgrade, no network improvement can breach. These are platform-level constraints built into the software architecture.

OrderSend() round-trip times are the most fundamental bottleneck. Documented measurements from MQL5 forums show MT4 typical execution times of 200 to 500 milliseconds, with one systematic test on a live ECN account recording a minimum of 280ms, a maximum of 2,130ms, and an average of 670ms. MT5 improves this to 60 to 200ms typical, with internal server latency of approximately 1 to 2ms. Even with a 0.5ms ping displayed in MT5’s status bar, actual trade execution logs show 40ms+ completion times. The ping measures only the network round-trip to the broker. The execution time includes broker gateway processing, trade server logic, bridge translation, and liquidity provider response. A trader who upgrades to a faster VPS reduces only the ping component while the platform overhead remains unchanged.

MT4 has a particularly punishing architectural limitation: a 30-second session timeout. After 30 seconds of inactivity on the trade connection, the next order requires re-authentication through the password database, adding approximately 500ms to execution with a documented range of 200 to 2,000ms. The standard workaround involves periodically modifying a dummy pending order to keep the session alive. The fact that this workaround exists and is widely documented on MQL5 forums illustrates how far the platform sits from HFT-grade infrastructure, where connections are maintained with dedicated heartbeat mechanisms operating in microseconds.

Tick dropping is by design, not a bug, and it is the single most disqualifying architectural fact. The official MQL4/MQL5 documentation confirms that if OnTick() is still processing when a new quote arrives, the new quote will be ignored. The EA never receives it. During volatile markets with rapid tick updates, EAs routinely miss price data. This is a deliberate design decision: MetaTrader prioritizes terminal responsiveness over complete data delivery. HFT systems using kernel bypass networking and FPGA parsing never miss a single message. Documented FPGA systems process NASDAQ TotalView-ITCH feeds at 8.5 million messages per second. MetaTrader’s OnTick() queue holds exactly one pending event.

MT4’s single trade context limitation means only one order operation can execute at a time across all EAs on the terminal. Multiple EAs attempting simultaneous trades trigger Error 146, “Trade context busy.” MT5 improves this to 8 concurrent trade contexts, a meaningful upgrade for retail multi-EA setups but irrelevant to HFT requirements. Institutional HFT systems process hundreds of thousands of orders per second with unlimited parallelism across dedicated execution threads, each connected to separate exchange ports.

MQL code execution speed compounds these constraints. MQL5 has been benchmarked at roughly 22 times slower than equivalent C++ code. MetaQuotes disputes the specific methodology of that benchmark, but the directional finding is consistent with what MQL is: a managed, sandboxed language with runtime bounds checking, no direct memory access, and no ability to interact with hardware or network interfaces at the kernel level. These safety features are appropriate for a retail trading terminal. They are the opposite of what speed-critical execution demands.

Broker-imposed message limits provide the final ceiling. MetaQuotes considers accounts exceeding 2,000 server messages per day “hyperactive.” IC Markets issues warnings at 3,000 messages per day and forcefully disables accounts at 15,000 messages per day. The practical maximum throughput on MT4 is approximately 2 to 5 orders per second. On MT5, perhaps 5 to 15 orders per second. An institutional HFT firm submitting 1,000 orders per second would exhaust MetaTrader’s entire daily message budget in 2 to 15 seconds. The platform was not designed for this volume and actively prevents it.

Six Orders of Magnitude: Where VPS Actually Sits in the Speed Hierarchy

The complete speed hierarchy reveals why “HFT VPS” is an oxymoron. Each tier operates in a fundamentally different time domain, separated by gaps that no incremental upgrade can close.

At the top, FPGA HFT colocation operates at 10 to 500 nanoseconds. The infrastructure is custom FPGA or ASIC hardware physically inside exchange data centers, connected via kernel bypass networking and direct market data feeds. The realistic strategies at this tier are market making and latency arbitrage between exchanges. The firms operating here spend millions per year and employ teams of hardware engineers.

Software HFT colocation operates at 1 to 10 microseconds. The infrastructure is optimized C++ with kernel bypass, colocated servers, and FIX API connections. Statistical arbitrage and optimal execution algorithms run at this tier. The latency is 1,000 to 10,000 times slower than FPGA but still 100 to 1,000 times faster than any retail setup.

Institutional algorithmic trading operates at 10 to 100 microseconds. Professional servers in proximity hosting with direct market access serve cross-venue arbitrage and professional market making. This tier is accessible to well-capitalized proprietary trading firms but not to retail traders using MetaTrader.

A premium retail VPS, colocated in the same Equinix facility as the broker with a cross-connect, achieves 0.3 to 2 milliseconds of network latency. This is the fastest infrastructure available to a retail MetaTrader trader. The realistic strategies here are scalping, news trading, and broker latency arbitrage. This tier delivers genuine, measurable value for active retail strategies.

A standard retail VPS in the same city or region as the broker operates at 5 to 20 milliseconds. This serves the vast majority of automated trading strategies: general EA trading, trend following, grid systems, and multi-pair scanning.

A home PC on good residential broadband sits at 50 to 200 milliseconds. Swing trading, position trading, and manual trading work fine at this latency. A home PC on poor internet connectivity runs at 100 to 500+ milliseconds, suitable only for position trading and not appropriate for any time-sensitive execution.

The numbers tell the story without commentary. The gap between the best retail VPS at 0.3ms and competitive HFT at 500 nanoseconds is 600x. Between a standard retail VPS at 10ms and top-tier FPGA systems at 50 nanoseconds, the gap is 200,000x. A retail VPS achieving “sub-millisecond latency” sounds impressive in marketing copy until you realize that HFT firms consider anything above a few microseconds uncompetitive.

The BIS Working Paper 955, the most rigorous academic study on HFT speed races, provides the definitive benchmark. Researchers analyzed latency arbitrage races on the London Stock Exchange and found that race times averaged approximately 80 microseconds, with winners beating losers by 5 to 10 microseconds. This is roughly 1,000 times faster than the best retail VPS setup. These races happen approximately 537 times per day on an average FTSE 100 stock. The entire race, from signal to filled order, completes in less time than a single MetaTrader OnTick() event takes to fire.

The Broker Execution Chain: The Bottleneck VPS Cannot Fix

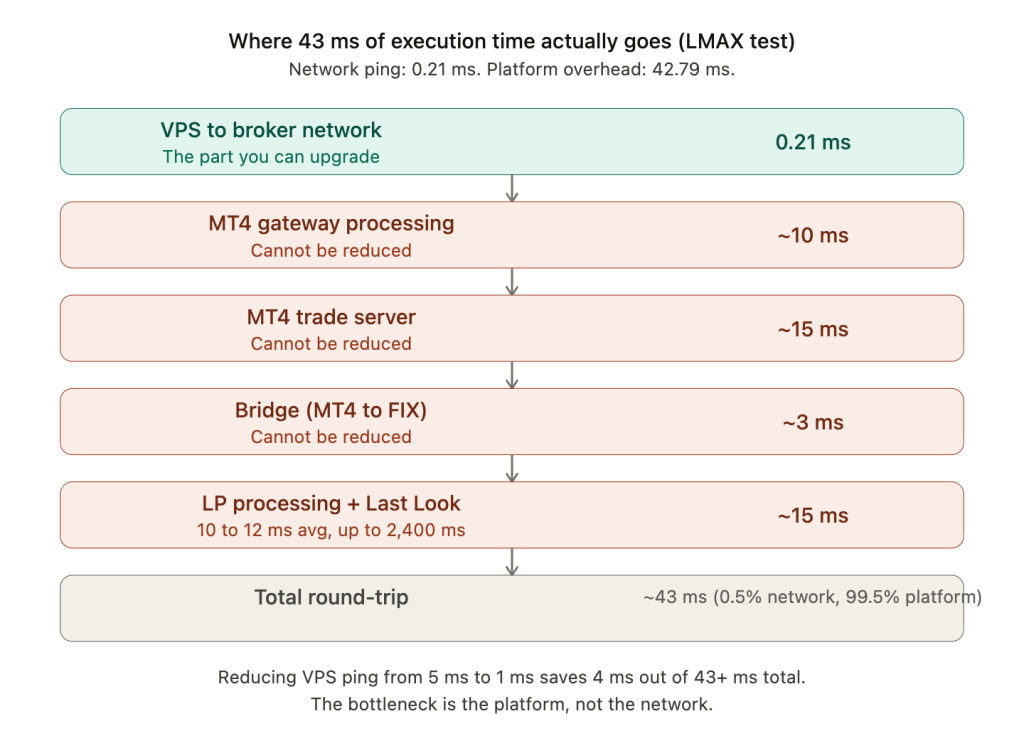

Even if network latency were zero, the broker-side execution chain imposes latency floors that no VPS upgrade can reduce. The full path from EA decision to filled order traverses at least seven steps: EA processing, MetaTrader client serialization, network transit, MT4/MT5 server reception, bridge translation from MetaTrader protocol to FIX, liquidity provider processing (including any Last Look hold), and the return confirmation through the same chain. Each step adds delay, and the platform and broker steps dominate the total.

A single measurement illustrates the problem. A test using LMAX Exchange, which executes 99.88% of orders in under 5ms, with a cross-connect ping of just 0.21ms, found that the MT4 gateway plus MT4 server plus bridge infrastructure added 43ms of total execution time. Almost the entire round-trip was platform overhead, not network delay. This is why obsessing over VPS network latency while running MT4 is optimizing the wrong variable. Reducing ping from 5ms to 1ms saves 4ms out of a total execution time that is 40ms+ regardless.

Last Look is the largest hidden variable in the execution chain. This mechanism allows liquidity providers a window to accept or reject trades after receiving the order, typically holding for 50 to 500ms before deciding. Current average hold times on major FX platforms run approximately 10 to 12 milliseconds, with thresholds recently reduced to 10 to 30ms on platforms like EBS and Cboe FX. But the averages disguise extreme variance. Analysis from The Full FX across 25 liquidity providers found response times ranging from zero to nearly 2.4 seconds, with one LP taking 110 times longer to reject orders than to accept them.

The LMAX Transaction Cost Analysis study documented the cost of Last Look with precision: even a 10ms hold time costs $15 per million traded, while 100ms costs $25 per million, with 60% of hold-time cost occurring in the first 10ms. A trader who upgrades from a 50ms VPS to a 5ms VPS saves nothing if their LP adds a 100ms Last Look hold. The VPS improvement disappears inside the broker-side overhead.

Broker execution speeds provide the practical floor. IC Markets reports an average execution speed of approximately 35ms on currency pairs. Pepperstone averages roughly 30ms. Independent testing by FXBrokersRanking across 7,547 Pepperstone trades found 82% had zero slippage, with 95.59% executing within a 50ms band. CompareForexBrokers tested 36 brokers and found total round-trips of 300 to 500ms from Australia, with the fastest brokers under 80ms broker-side. These figures represent the practical floor for retail execution regardless of VPS quality.

The bridge layer, software from providers like PrimeXM, oneZero, or Gold-i that translates MetaTrader orders into FIX protocol for liquidity providers, adds another 1 to 5ms minimum. Tools for Brokers claims 1ms bridge execution speed with total MT5 cycle under 5ms, though independent verification is scarce.

The realistic best-case total round-trip through a colocated VPS with MT5 and an ECN broker offering firm liquidity (no Last Look) is approximately 11ms. Through MT4 with a Last Look liquidity provider, the range extends to 67 to 800ms. Both figures are measured in milliseconds. HFT operates in nanoseconds and microseconds. The broker execution chain alone, before any network latency is added, places retail trading in a time domain that is four to six orders of magnitude slower than institutional HFT. No VPS can change this because the bottleneck is not the network. It is the platform and the broker.

What Retail Traders Actually Mean by “HFT” and What VPS Providers Sell

Searching MQL5 Market for “HFT” reveals what retail traders actually buy under this label. The results fall into three categories: prop firm challenge passers that burst-trade US30 during the New York open for 15 to 30 minutes, scalping EAs mislabeled as HFT that use grid systems with ATR-based position sizing, and latency arbitrage bots that exploit price lag between fast and slow brokers. None of these execute more than a few hundred trades per day. A documented ForexFactory journal running a “HFT” gold grid EA averaged 3,000 to 4,000 trades per month, roughly 150 per day, or approximately 100,000 times slower than institutional HFT firms that execute millions of orders daily.

The marketing creates a false equivalence through a simple logical chain: HFT firms need low latency, VPS providers offer low latency, therefore VPS enables HFT. Each link in this chain is technically true in isolation. The conclusion is false because it ignores six orders of magnitude between “low latency for retail” (milliseconds) and “low latency for HFT” (nanoseconds). It also ignores that latency is only one of dozens of requirements, alongside custom hardware, exchange colocation, direct market data feeds, proprietary protocols, regulatory authorization, and millions in capital.

Specific provider claims illustrate the problem. TradingFXVPS explicitly states on their HFT product page that “your trades can compete with even the fastest HFT companies in the world.” This is flatly false by every metric documented in this article: speed, message volume, infrastructure, regulatory status, and capital requirements. VPS-Mart uses “HFT” over 20 times on a single marketing page while targeting MT4/MT5 users. MassiveGRID published content about choosing VPS “for traders executing thousands of trades per second” while serving a platform that physically cannot process more than 5 to 15 orders per second.

This is not a minor semantic complaint. Traders who believe they are running HFT strategies may make infrastructure and risk management decisions based on that false premise. A trader who thinks their grid EA is “high-frequency” may undersize their VPS because HFT implies light, fast code rather than the position-accumulating, memory-intensive reality of grid systems. They may overspend on sub-millisecond network improvements that produce zero measurable benefit for a strategy trading 150 times per day on M5 charts.

The honest framing is straightforward. What retail traders call “HFT” is really high-frequency-for-retail: active scalping or grid strategies that trade dozens to hundreds of times per day rather than the handful of trades per week that a swing strategy produces. This is legitimate algorithmic trading that genuinely benefits from VPS hosting. The uptime, the reduced latency compared to home internet, the stability during news events, all of these deliver real value for active retail strategies. But this activity operates in a completely different speed regime than institutional HFT, and calling it HFT creates expectations that no VPS can fulfill.

The distinction also matters for strategy development. A retail trader pursuing “HFT” on MetaTrader may spend months optimizing for microsecond improvements that the platform cannot deliver, rather than focusing on the factors that actually determine retail profitability: strategy edge, risk management, position sizing, and execution quality at the millisecond scale where their platform actually operates.

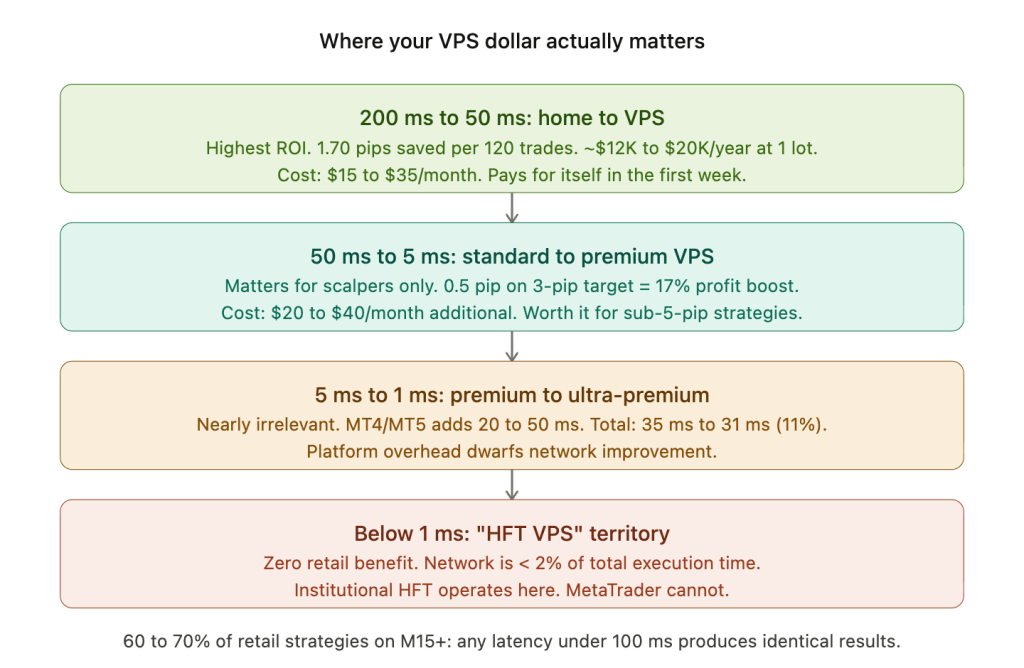

The Diminishing Returns Curve: Where Your VPS Dollar Actually Matters

The economics of speed follow a clear diminishing returns pattern. Understanding where the curve breaks prevents both underspending (running on a home PC when a VPS would pay for itself) and overspending (chasing sub-millisecond improvements that produce no measurable benefit on MetaTrader).

Moving from 200ms to 50ms saves real money. This is the home-internet-to-VPS transition, and it is the single highest-ROI speed investment a retail trader can make. The ForexVPS.net London-versus-NYC experiment documented a 1.70-pip cumulative slippage difference over 120 trades between a sub-1ms London VPS and a 75ms NYC VPS. Scaled to 1 standard lot monthly, this represents roughly $12,000 to $20,400 annually in avoidable slippage. This experiment was published by a VPS provider with commercial interest and has not been independently replicated, but the directional finding, closer VPS means less slippage, is consistent with broker execution data and market microstructure research. For any trader running an EA that executes more than a handful of trades per month, a VPS in the same data center as the broker pays for itself many times over.

Moving from 50ms to 5ms matters for scalpers and only for scalpers. Traders targeting 2 to 3 pips per trade see meaningful slippage reduction in this range. When the profit target is 3 pips, a 0.5-pip slippage improvement from better latency represents a 17% boost to net profit per trade. Over hundreds of trades per month, this compounds significantly. The cost of this improvement, upgrading from a standard VPS to a premium Equinix-colocated plan, is typically $20 to $40/month additional.

Moving from 5ms to 1ms is nearly irrelevant for retail trading. MT4/MT5 processing itself adds 20 to 50ms to every order regardless of network latency. Improving network transit from 5ms to 1ms when the platform adds 30ms changes total execution from 35ms to 31ms, an 11% improvement in total time that is practically invisible in trading results. The cost of chasing sub-millisecond latency (dedicated cross-connects, premium hosting tiers) is not justified by the execution improvement for any MetaTrader-based strategy.

Below 1ms, there is zero retail benefit. The platform overhead dominates. Every millisecond saved on the network disappears into the 20 to 50ms of MetaTrader processing, the 10 to 12ms of average Last Look hold time, and the 1 to 5ms of bridge translation. Spending more for 0.5ms improvement when the total chain adds 40ms+ is optimizing a component that represents less than 2% of total execution time.

The spread provides the ultimate floor for speed relevance. If EUR/USD spread is 1 pip, a strategy targeting 10+ pips loses only 1 to 3% of its profit target to 0.1 to 0.3 pips of slippage. Speed barely matters. A strategy targeting 2 to 3 pips loses 17 to 25% to the same slippage. Speed is critical. A strategy targeting 1 pip or less is competing with the spread itself and cannot reliably profit at retail regardless of speed because the spread consumes most of the profit target before execution quality even enters the equation.

The practical conclusion: for the roughly 60 to 70% of retail strategies operating on M15 or higher timeframes with targets above 10 pips, any latency under 100ms produces functionally identical results. A $15/month VPS in the right data center delivers the same execution quality as a $70/month premium plan for these strategies. The premium plans earn their cost only for the approximately 10% of retail strategies that scalp on M1 to M5 with sub-5-pip targets, where the 50ms-to-5ms improvement translates directly to better fills.

What a VPS Genuinely Delivers

A forex VPS provides real, measurable value for retail algorithmic trading. The value has nothing to do with HFT and everything to do with five operational advantages that no home setup can reliably match.

The primary value is 24/7 uptime. EAs need to run continuously through the 120-hour trading week without interruption from power outages, internet disconnections, Windows Update restarts, or household disruptions. A VPS with 99.99% uptime permits a maximum of 52 minutes of downtime per year. A home PC with residential internet delivers 90 to 97% compounded availability, translating to 263 to 876 hours of potential downtime annually. For any EA managing positions with client-side logic, trailing stops, grid levels, dynamic stop management, this uptime difference is not a convenience. It is the infrastructure foundation that determines whether the EA can function as designed.

Slippage reduction for active traders is the second value, and it is quantifiable. The documented 1.70-pip improvement over 120 scalping trades from a colocated VPS versus a remote connection represents real money. For traders executing dozens to hundreds of trades monthly on sub-H1 timeframes, a VPS in the same data center as the broker pays for itself in reduced slippage within the first month.

News event continuity is the third value. Home internet connections degrade during major economic releases when global financial data traffic surges. VPS connections within Equinix facilities bypass public internet entirely via dedicated cross-connects, maintaining stable latency through NFP, FOMC, and CPI releases while home connections experience congestion and packet loss.

Multi-platform reliability is the fourth value. Running several MT4/MT5 instances consistently across the trading week requires more stability than a home PC typically provides. A VPS handles 2 to 8 terminal instances with dedicated resources that do not compete with browsers, operating system updates, or other desktop applications.

Meaningful speed advantage for the approximately 10% of retail strategies that are genuinely latency-sensitive is the fifth value. Scalping EAs on M1 to M5, news reaction bots, and broker latency arbitrage strategies all benefit measurably from sub-5ms network latency to the broker. For these specific strategies, a premium VPS with Equinix colocation delivers execution quality that a home connection cannot approach.

The strategies that thrive on VPS infrastructure are not HFT. They are medium-frequency trading at 10 to 100 trades per day on M5 to M15 timeframes, statistical arbitrage between correlated pairs operating on second-to-minute timescales rather than microseconds, session-based breakout strategies that need reliable execution at specific market hours, and grid systems where uptime matters infinitely more than the difference between 2ms and 0.5ms latency. The most commercially successful EAs on MQL5 Signals trade 15 to 70 times per month on M5 to H4 timeframes. They are not labeled “HFT.” They succeed because their strategies have an edge that reliable infrastructure allows them to capture consistently.

For purchasing decisions, three tiers cover the realistic retail spectrum. MetaQuotes’ built-in VPS at $12.80 to $15/month achieves sub-3ms latency to 70% of broker servers and is sufficient for the majority of retail strategies that do not require DLL support, RDP access, or multiple accounts. BeeksFX, publicly traded on the London Stock Exchange as BKS and therefore the most independently verifiable provider, offers SLAs under 1ms via direct Equinix cross-connect from roughly $31/month. ForexVPS.net and FXVM offer Equinix-colocated hosting from $35/month with claimed sub-1ms latency to popular brokers. Any of these delivers the full retail speed advantage. None of them delivers HFT. The honest providers do not claim to.

FAQ

If HFT on a VPS is impossible, why do so many VPS providers market “HFT” products?

Because the term has no legal definition in the United States, and the marketing works. “HFT VPS” implies cutting-edge speed and attracts traders who want the fastest possible execution. The products themselves are standard low-latency VPS plans, which genuinely deliver value for active retail trading. The marketing is misleading not because the product is bad but because the label creates false expectations. A VPS marketed as “low-latency hosting for active MetaTrader strategies” would be equally accurate and far more honest, but “HFT” generates more clicks. Evaluate providers on their actual specifications (latency to your specific broker, uptime SLA, virtualization technology, data center location) rather than on speed-related branding.

What about latency arbitrage EAs that exploit price differences between brokers? Is that HFT?

Latency arbitrage between retail brokers is a legitimate strategy that benefits from VPS hosting, but it is not HFT by any regulatory or institutional definition. These EAs exploit the delay between a fast-feed broker and a slow-execution broker, typically operating with holding times of seconds to minutes and executing dozens to low hundreds of trades per day. Institutional latency arbitrage operates between exchanges at microsecond speeds with custom hardware. The retail version works on a fundamentally different timescale and against a fundamentally different counterparty (a retail broker rather than an exchange order book). It also faces a practical ceiling: brokers actively detect and restrict latency arbitrage activity. IC Markets, Pepperstone, and most ECN brokers monitor for this pattern and may revoke accounts that engage in it systematically.

My EA executes 200 trades per day. Is that high-frequency?

By retail standards, 200 trades per day is very active. By institutional HFT standards, it is roughly 100,000 times slower. A useful benchmark: the most active institutional HFT firms submit millions of orders per day on a single instrument, with the majority cancelled within milliseconds. MetaQuotes considers 2,000 server messages per day “hyperactive,” and IC Markets disables accounts at 15,000 messages per day. At 200 trades per day with associated modifications and cancellations, you are operating well within normal retail parameters. Your strategy benefits from VPS uptime and reduced latency, but calling it HFT creates infrastructure expectations that MetaTrader cannot fulfill.

Should I switch from MetaTrader to a FIX API connection for better speed?

A FIX (Financial Information eXchange) API connection bypasses MetaTrader entirely and connects directly to the broker’s execution infrastructure. This eliminates the MT4/MT5 platform overhead (20 to 50ms) and the bridge translation layer (1 to 5ms), reducing total execution time to approximately 5 to 15ms on a well-configured setup versus 35 to 100ms+ through MetaTrader. The tradeoff is substantial: FIX API requires custom software development in C++, Python, or Java; it eliminates the entire MQL ecosystem of indicators, EAs, and visual charting; it demands direct broker relationships (not all brokers offer FIX access to retail clients); and it requires significantly more technical expertise to deploy and maintain. For the approximately 1 to 2% of retail traders who have the development skills and a strategy that genuinely benefits from sub-10ms execution, FIX API is the correct next step beyond MetaTrader. For everyone else, the platform overhead is an acceptable cost for the ecosystem it provides.

Is a dedicated server better than a VPS for speed-sensitive trading?

A dedicated server eliminates the noisy neighbor problem of shared VPS plans by giving you the entire physical machine. This matters during high-volatility events when every trader on a shared host activates simultaneously and CPU steal can spike from under 1% to 5 to 15%. But a dedicated server does not change the MetaTrader platform overhead, the broker execution chain, the bridge latency, or the Last Look mechanism. It improves the VPS layer while leaving the dominant bottlenecks untouched. For scalping strategies where dedicated CPU cores during news events matter, a dedicated server at $100 to $200/month provides genuine benefit. For strategies trading on M15 or higher timeframes, the $70 to $150/month premium over a VPS buys infrastructure headroom that produces no measurable execution improvement.

How do prop firms that advertise “HFT allowed” relate to actual HFT?

Prop firm challenges that allow “HFT” are using the term to mean “high trade frequency relative to other retail traders,” not institutional HFT. These challenges typically permit burst trading of 50 to 200 trades during a short session window, often on indices like US30 during the New York open. The EAs sold for these challenges on MQL5 Market are grid systems and scalpers that fire rapidly for 15 to 30 minutes, pass the profit target, then stop. This is aggressive retail scalping with concentrated execution timing. It benefits from a VPS for reliability during the burst window, but the trade frequency is still orders of magnitude below institutional HFT, and the execution infrastructure is standard MetaTrader on a standard VPS.

References

- U.S. Securities and Exchange Commission. Concept Release on Equity Market Structure (2010): five functional characteristics of HFT (extraordinary speed, colocation, short holding times, mass order submission/cancellation, end-of-day flat positions). NASDAQ order-to-trade ratio data: HFT firms averaging 11.2:1, representing 32% of dollar volume and 94% of order messages. Virtu Financial annual report (2024 10-K): $236.4 million communication and data processing expenses, $27.7 million microwave network joint venture payments.

- European Securities and Markets Authority / MiFID II. Article 4(1)(40): definition of high-frequency algorithmic trading (colocation/proximity, system-determined execution, high message intraday rates). Commission Delegated Regulation 2017/565: quantitative thresholds (2 messages/second/instrument, 4 messages/second across all instruments). Requirement for HFT practitioners to be authorized as investment firms.

- Congressional Research Service. Report on high-frequency trading: “imprecise catchall term that currently has no legal or regulatory definition” in the United States.

- Bank for International Settlements. Working Paper 955: latency arbitrage races on the London Stock Exchange, average race time approximately 80 microseconds, winners beating losers by 5 to 10 microseconds, approximately 537 races per day on an average FTSE 100 stock.

- IEEE Xplore. Published FPGA latency measurement: average tick-to-trade latency of 480 nanoseconds. Top-tier FPGA systems achieving single-digit to double-digit nanosecond execution.

- Exchange Colocation Pricing. CME Group Aurora facility: $15,500 to $19,000/month cabinet rental. ICE Chicago: $3,300 to $12,000/month depending on power allocation. NYSE 10-gigabit LCN port pair: $15,500/month. Cross-connect pricing: $500 to $15,500/month per connection depending on port speed and exchange.

- Exegy. Market data infrastructure cost analysis: $4.74 million to build full North American market data coverage, $3.5+ million per year to maintain. OPRA options data feed requiring 40 to 100 Gbps networking infrastructure.

- MQL5.com Forum and Documentation. OrderSend() execution measurements: MT4 typical 200 to 500ms (systematic ECN test: min 280ms, max 2,130ms, avg 670ms). MT5 typical 60 to 200ms, internal latency ~1 to 2ms. MT4 30-second session timeout adding ~500ms re-authentication. OnTick() tick-dropping behavior confirmed in official documentation. MT4 single trade context (Error 146), MT5 upgraded to 8. MQL5 benchmarked at ~22x slower than C++ (methodology disputed by MetaQuotes). MetaQuotes “hyperactive” account threshold at 2,000 messages/day.

- LMAX Exchange. Execution data: 99.88% of orders filled under 5ms. Cross-connect test: 0.21ms ping, 43ms total execution time demonstrating platform overhead dominance. Transaction Cost Analysis whitepaper (84 pages, 7.1 million orders): Last Look costs $15/million at 10ms hold, $25/million at 100ms, 60% of cost in first 10ms, zero price improvement on last-look feeds.

- The Full FX. Analysis of 25 liquidity providers: Last Look response times ranging from zero to 2.4 seconds, one LP taking 110x longer to reject than accept. Current average hold times 10 to 12ms on major platforms.

- Broker Execution Data. IC Markets: ~35ms average execution, account warnings at 3,000 messages/day, forced disabling at 15,000/day. Pepperstone: ~30ms average execution. FXBrokersRanking: 7,547 Pepperstone trades, 82% zero slippage, 95.59% within 50ms band. CompareForexBrokers: 36 brokers tested, 300 to 500ms total round-trip from Australia, fastest under 80ms broker-side. Tools for Brokers: 1ms bridge execution claim, MT5 cycle under 5ms (independent verification scarce).

- VPS Provider Claims and Data. TradingFXVPS: “your trades can compete with even the fastest HFT companies in the world” (documented on HFT product page). VPS-Mart: “HFT” used 20+ times on single marketing page. MassiveGRID: content referencing “thousands of trades per second” for MT4/MT5 users. ForexVPS.net: London-versus-NYC slippage experiment (1.70 pips over 120 trades, published by provider with commercial interest, not independently replicated). BeeksFX (LSE: BKS): SLAs under 1ms, Equinix cross-connect, from ~$31/month.

- Academic Research. Approximately 96% of trading orders on US equity exchanges cancelled, ~40% within 500 milliseconds. HFT contributing 80%+ of limit order messages on NASDAQ-OMX Stockholm. Kernel bypass networking (Solarflare OpenOnload, DPDK): 1 to 10 microsecond latency. FPGA custom firmware development: $1 to $5 million over 6 to 18 months. Custom ASIC fabrication: ~$30 million per run.

Editorial Note

This article examines whether high-frequency trading can run on a retail forex VPS by comparing the infrastructure, speed, cost, and regulatory requirements of institutional HFT against the technical capabilities of MetaTrader on a virtual private server. It does not constitute financial advice, trading strategy recommendations, or endorsement of any specific VPS provider, broker, or trading approach.

The article concludes that genuine HFT is physically impossible on a retail VPS running MetaTrader, based on documented platform limitations (OrderSend() latency, tick dropping, message rate ceilings), broker-side execution chain overhead, and the four-to-six-order-of-magnitude speed gap between institutional FPGA/colocation infrastructure and retail VPS hosting. This conclusion is consistent with SEC and MiFID II functional descriptions of HFT, the BIS Working Paper on latency arbitrage, and MetaQuotes’ own platform documentation.

Specific VPS provider marketing claims are quoted directly from publicly accessible product pages as of March 2026. The article does not claim that the underlying VPS products are defective. It claims that marketing them as enabling HFT creates a false equivalence that may lead traders to make suboptimal infrastructure and risk management decisions.

The ForexVPS.net slippage experiment (1.70 pips over 120 trades) was published by a VPS provider with commercial interest in demonstrating VPS value and has not been independently replicated. The directional finding is consistent with broker execution data and market microstructure research, but the specific figures should be treated as indicative rather than guaranteed outcomes.

This article runs on a website operated by a VPS provider. The editorial decision to publish content establishing that HFT is impossible on the provider’s own product reflects a commitment to accurate technical information over marketing claims. The genuine value of a forex VPS for retail algorithmic trading, documented throughout this article and the broader site, is substantial and well-supported by evidence. It does not require HFT terminology to justify.