The BIS 2025 Triennial Survey reports forex turnover reached $9.6 trillion per day in April 2025, up 28% from $7.5 trillion in 2022. The USD appears on one side of 89.2% of all trades. Spot FX alone accounts for $3 trillion per day. This is the market that retail algorithmic traders operate in, and the infrastructure between their algorithm and the matching engine determines whether their orders arrive at the price they intended or the price that remains after everyone has already traded.

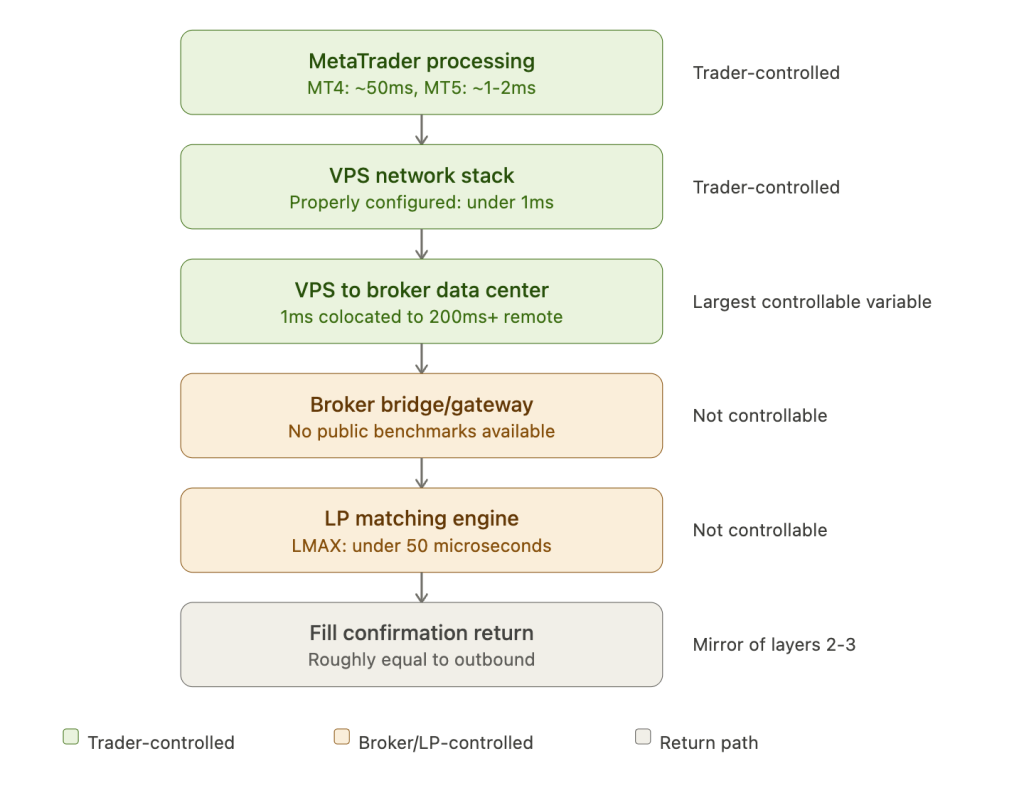

Between an EA deciding to buy and the broker confirming the fill, the order passes through seven distinct layers: MetaTrader’s internal processing, the Forex VPS network stack, the network path to the broker’s data center, the broker’s bridge and gateway, the liquidity provider’s matching engine, and the return path for fill confirmation. Each layer adds latency. Academic research quantifies the stakes: Moallemi and Saglam (2013, Operations Research) proved that reducing latency from 500ms to 5ms cuts the cost of immediacy to just 5% of its original value. The marginal benefit of each millisecond removed increases as total latency approaches zero.

For retail traders, this does not mean chasing microsecond advantages. It means understanding which layers are controllable (VPS location, platform choice, configuration) and which are not (broker bridge processing, LP matching engine speed, last look windows). A trader who moves from a home PC to a colocated VPS eliminates 100 to 200ms of controllable latency. A trader who then switches from MT4 to MT5 eliminates another 48ms of platform processing overhead. Beyond that, further improvement requires bypassing MetaTrader entirely via FIX API, which is a different infrastructure category with different costs.

This article maps the complete infrastructure stack for retail forex algorithmic trading: the execution chain with latency at each layer, data center geography, VPS architecture, uptime math, broker execution models, security and monitoring, and the cost-latency curve. Specialized articles on this site go deeper into each territory. This is the reference map.

The execution chain: from algorithm to fill

The full path from algorithm decision to confirmed fill crosses six distinct infrastructure layers, each with measurable latency. Understanding where time is spent reveals which improvements are worth pursuing and which are marketing noise.

The first layer is the trading platform itself. When an EA calls OrderSend(), MetaTrader does not instantly transmit the request. MT4 performs internal processing that adds approximately 50ms of latency before the order reaches the network. This figure comes from an MQL5 forum administrator and is consistent across multiple independent forum measurements. MT5 reduces this to approximately 1 to 2ms through architectural improvements, a 48ms advantage that compounds across every order. MT4 has an additional quirk that catches traders who run EAs with infrequent trading: a 30-second session timeout triggers re-authentication on the next OrderSend(), adding 200 to 2,000ms to that specific order. This timeout is documented by ForexFactory developer “rooicol” and widely confirmed. MT4’s OrderSend() is synchronous and blocks the EA thread until the broker responds. MT5’s OrderSendAsync() returns immediately, freeing the EA to continue processing while the order is in flight.

The second layer is the VPS network stack. On a properly configured system, this adds less than 1ms. On a shared VPS with CPU contention, Windows overhead from Nagle’s algorithm, or antivirus file scanning, this can reach 10 to 15ms. Platform-level optimization (covered in our MT4 VPS optimization guide) keeps this layer negligible.

The third layer is the network path from VPS to the broker’s data center. This is the largest controllable variable in the entire chain. A colocated VPS in the same Equinix facility as the broker achieves under 1ms (with cross-connect claims of 0.3 to 0.5ms from VPS providers). A same-city VPS reaches 5 to 20ms. A standard remote VPS in the same region runs 20 to 50ms. Home broadband adds 50 to 200ms, and intercontinental connections reach 100 to 300ms or more. The physics floor is fiber optic transmission at approximately 200,000 km per second, roughly 5 microseconds per kilometer. A transatlantic New York to London path has a theoretical minimum of approximately 55ms, with commercial routes running approximately 70ms.

The fourth layer is the broker’s bridge and gateway. Major bridge providers include PrimeXM (XCore), oneZero (Hub), Gold-i, and Takeprofit Tech. PrimeXM claims “sub-millisecond connectivity” when colocated in LD4, NY4, or TY3. oneZero operates a C++ architecture with dedicated hosted instances. No independently verified bridge latency figures were found in public sources during research for this article. Bridge providers universally avoid publishing specific benchmarks. The 8 to 15ms range suggested in some existing articles could not be verified from primary sources. What the bridge does is well-documented: liquidity aggregation (assembling best bid and offer from multiple LPs), markup application, A/B book routing decisions, risk management, and credit checks. A well-built STP stack can forward to the LP matching engine in under 100 microseconds. A poorly built one introduces chronic slippage.

The fifth layer is the liquidity provider’s matching engine. LMAX Exchange, the retail benchmark for transparent FX execution, publishes internal exchange latency of under 50 microseconds and average trade latency including network of under 3ms. LMAX operates matching engines in London (LD4), New York (NY4), Tokyo (TY3), and Singapore (SG1), each handling 40,000 orders per second. LMAX operates with no last look, offering firm liquidity on a central limit order book. Modern ECN matching engines generally confirm fills in 150 to 300 microseconds round-trip. These are not numbers that retail infrastructure can meaningfully influence.

The sixth layer is the return path. Fill confirmation travels back through the same network, adding roughly equivalent latency to the outbound leg. MetaTrader processes OnTradeTransaction events asynchronously after OrderSend returns.

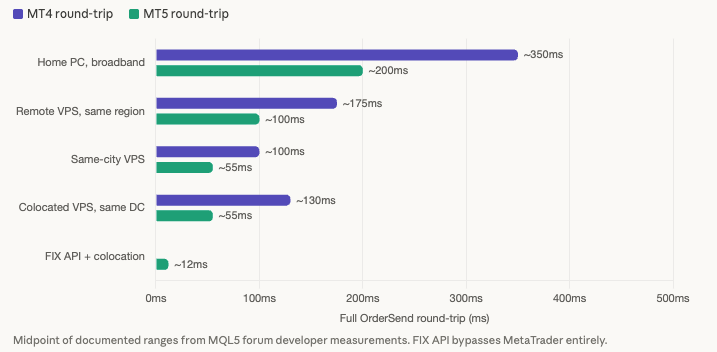

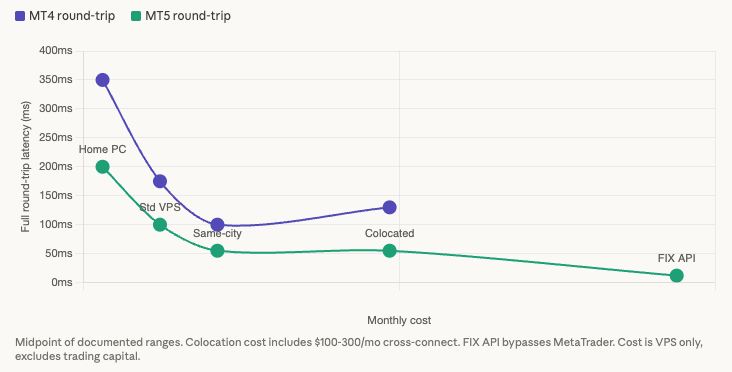

Realistic full round-trip times measured by MQL5 forum developers paint the practical picture. A home PC on broadband produces 200 to 500ms on MT4 and 100 to 300ms on MT5. A remote VPS in the same region runs 100 to 250ms on MT4 and 50 to 150ms on MT5. A colocated VPS in the same data center achieves 60 to 200ms on MT4 and 30 to 80ms on MT5. One user at Equinix NY measured 40ms per trade on MT5. FIX API with colocation bypasses MetaTrader entirely, achieving 5 to 20ms. The critical insight embedded in these numbers: even with sub-1ms network ping, broker server-side processing (bridge, matching, risk checks) adds a minimum of 30 to 60ms for retail MT4/MT5 accounts. The gap between a colocated VPS and FIX API is not about network latency. It is about bypassing MetaTrader’s processing overhead.

During news events, the entire chain degrades. Liquidity providers withdraw or widen quotes dramatically. Broker processing time increases as server queues build with order volume spikes. MQL5 forum moderator William Roeder (32,000+ posts) noted that execution “can take minutes to do a trade because of the servers during news.” Forum measurements during volatile conditions range from 3,000 to 6,000ms per trade, with one extreme case reaching 150,063ms (2.5 minutes) for a single OrderSend on MT5.

Where the infrastructure lives: data centers and colocation

Forex has no single exchange. Unlike equities, where the NYSE or Nasdaq has a specific physical location, forex execution is distributed across dozens of liquidity providers and broker matching engines in data centers worldwide. Colocation in forex means proximity to the broker’s trade server and LP aggregation point, not to a central exchange. The target is sub-millisecond to low single-digit millisecond latency, not the microsecond advantages that equity HFT firms chase.

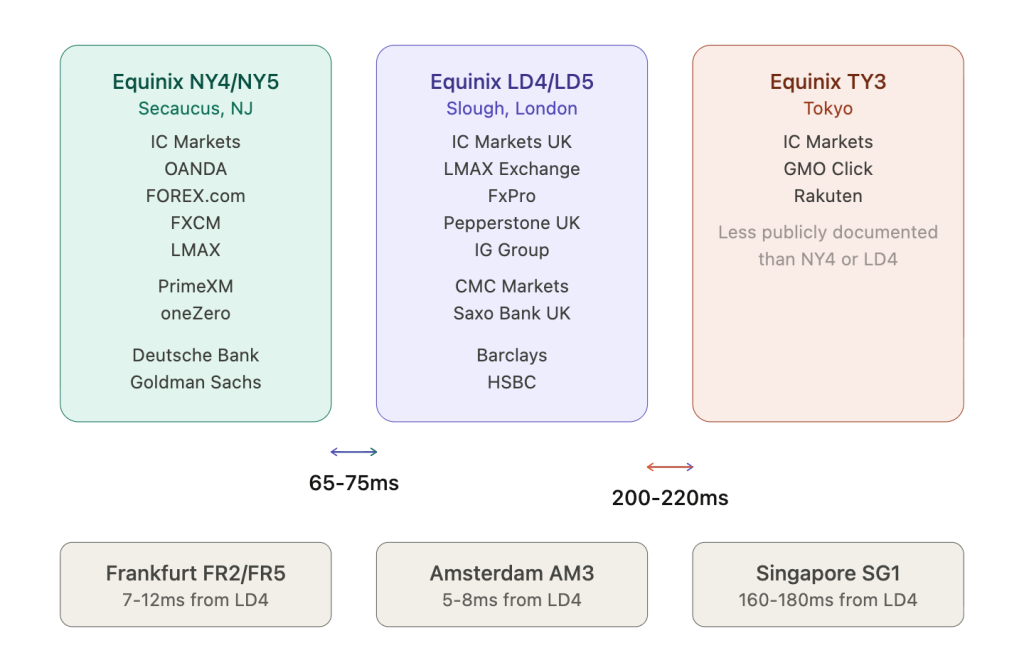

Three Equinix facilities function as gravitational hubs for the majority of retail forex infrastructure.

Equinix NY4 and NY5 in Secaucus, New Jersey are the center of electronic trading in the Americas. When a broker states “New York servers,” they almost certainly mean NY4 or NY5. Brokers with confirmed presence include IC Markets (official website states “collocated in the Equinix NY4 Data Centre”), OANDA (listed by Beeks Group and multiple VPS providers), FOREX.com/StoneX (confirmed across multiple sources), and FXCM (explicitly states NY4 and LD5). Interactive Brokers and LMAX appear on the Beeks NY5 cross-connect list with medium confidence. Major bank liquidity providers on the same Beeks cross-connect list include Deutsche Bank, Barclays, Goldman Sachs, UBS, HSBC, and Morgan Stanley. Bridge providers PrimeXM and oneZero are both confirmed at NY4. Latency benchmarks from NYCServers (a commercially interested VPS provider) show sub-2ms ping to IC Markets (1.03ms), Pepperstone (1.03ms), OANDA (0.98ms), and FXCM (1.02ms) from NY4-area infrastructure.

Equinix LD4 and LD5 in Slough, west of London, are the European equivalent. The two facilities sit approximately 100 meters apart on the same campus with fiber cross-connects between them. IC Markets UK mentions LD5 on its official site. LMAX Exchange moved into LD4 in Q4 2012 according to independent data center broker Colo-X. FxPro deployed a “dedicated physical cross-connect within Equinix LD4” per an FX News Group press release. Pepperstone UK, IG Group, CMC Markets, FXCM, Saxo Bank UK, Tickmill UK, and Admirals are listed by MassiveGRID with medium confidence. Cross-facility latency from LD4 reaches Frankfurt (FR2/FR4) in 7 to 12ms, Amsterdam (AM3) in 5 to 8ms, NY4 in 65 to 75ms, and TY3 in 200 to 220ms. These cross-facility figures come from MassiveGRID, a commercially interested source.

Equinix TY3 in Tokyo serves as the primary hub for Asia-Pacific. Japan is the world’s largest retail FX market by volume, yet less publicly available broker-specific information exists for TY3 compared to NY4 or LD4. IC Markets is confirmed present. GMO Click and Rakuten Securities are referenced but specific TY3 confirmation is weaker. Frankfurt (FR2/FR5) houses German banks and LMAX EU presence at 7 to 12ms from London. Singapore (SG1), the world’s third-largest forex trading center, presents a paradox: most MAS-regulated brokers (IG, OANDA) do not host trade servers in Singapore but instead route through London, adding 160 to 180ms.

The distinction between a cross-connect and internet routing determines whether “same data center” translates into sub-millisecond latency or merely low single-digit. A cross-connect is a direct physical fiber cable between two racks within the same facility, eliminating all public internet routing. It achieves approximately 0.1 to 0.5ms and costs $100 to $300 per month. A “same-facility VPS” without a cross-connect still benefits from proximity but relies on internal data center networking, typically under 1ms but less consistent than a dedicated fiber path.

Most brokers are vague about their data center locations. Only IC Markets and FxPro publish specific facility names on their official websites. Pepperstone’s infrastructure documentation is described as “notably vague” in independent analysis. Many smaller brokers say “London servers” without specifying the facility, making it impossible to verify whether a VPS in LD4 achieves the expected latency benefit. The practical approach: use traceroute and IP geolocation (ipinfo.io) to identify the city and data center from the broker server IP visible in MetaTrader’s connection settings. Contact broker support directly. Check VPS provider broker latency databases. Verify before committing to a VPS location.

The VPS layer: architecture that matters

The marketing specifications on a VPS product page (4 vCPU, 8 GB RAM, 100 GB NVMe) describe the theoretical allocation. Whether the trading terminal actually receives those resources during a volatile London session depends on three architectural decisions the provider made: the hypervisor, the overcommit ratio, and the storage backend.

KVM is the preferred hypervisor for trading VPS deployments. It is a Type 1 hypervisor that provides true hardware isolation. Each virtual machine runs its own kernel with dedicated CPU, RAM, and disk controllers. When a provider allocates 4 vCPU cores, KVM maps them to specific physical cores. Overhead versus bare metal is approximately 1 to 3%. KVM supports Windows Server natively, which is essential for MetaTrader. Hyper-V, Microsoft’s own Type 1 hypervisor, is acceptable. It offers deep Windows integration and dynamic memory management. Both KVM and Hyper-V provide genuine isolation between virtual machines. OpenVZ and LXC are OS-level containerization technologies that share the host Linux kernel. They cannot run Windows natively, making them unsuitable for MetaTrader. Resources on OpenVZ are frequently oversold because the shared kernel makes overcommit trivially easy for providers.

The noisy neighbor problem occurs when multiple virtual machines compete for shared physical resources. The diagnostic metric is CPU Ready time: the duration a VM wants to execute but the hypervisor has no physical core available. A CPU Ready time exceeding 5% or 2,000ms indicates the host is overcommitted. On Windows, inconsistent response times in Task Manager during periods when the VPS should be idle are the visible symptom. On Linux, the vmstat command reports steal time, and sustained values above 5% confirm real contention. KVM isolation is better than containerization, but KVM can still be oversold. The discipline is on the provider, not inherent in the technology. Multiple Myfxbook forum users reported VPS slowdowns on 6 to 14 GB plans with adequate RAM. The root cause was shared CPU, and dedicated cores resolved the issue. For scanner workloads that must process ticks reliably during high-volatility events, dedicated CPU resources are worth the premium.

Memory ballooning is an invisible performance threat. The hypervisor’s balloon driver inside the guest OS “inflates,” claiming memory pages from the guest and returning them to the host when the physical server is under pressure. The escalation path is predictable: transparent page sharing first, then ballooning, then memory compression, then swap to disk, then performance collapse. The insidious characteristic: ballooning often does not trigger standard monitoring alerts. The provider’s dashboard shows normal host-level memory while the guest VM is thrashing internally. The first thing ballooning destroys is the filesystem cache, which is the exact layer that keeps MetaTrader’s I/O performance acceptable for chart loading and journal writes.

Storage technology affects three specific MetaTrader operations. NVMe SSD delivers 2,000 to 7,000 MB/s sequential throughput with 500,000 to 800,000 IOPS at 10 to 20 microsecond latency, using PCIe directly. SATA SSD is limited by the SATA III interface to approximately 550 MB/s and 90,000 to 100,000 IOPS at 100 to 150 microsecond latency. The difference matters for startup recovery after crashes or reboots (loading chart history and EA configurations), journal writes that accumulate hundreds of megabytes to gigabytes over months of operation, and backtesting with heavy disk I/O (though backtesting should never run on a live trading VPS, as covered in our MT4 vs MT5 comparison).

How to verify what you are actually getting: Geekbench 6 for CPU (target 1,500+ single-core score), CrystalDiskMark for disk throughput on Windows, and ping combined with tracert to measure latency to the broker’s server IP. Run these benchmarks immediately after provisioning a new VPS and periodically thereafter. Degradation over time suggests the provider is adding more tenants to the same physical host.

Uptime: the math of always-on trading

SLA percentages are abstract until converted to downtime. A 99.9% uptime guarantee allows 8 hours and 46 minutes of downtime per year, or approximately 43 minutes per month. That is enough to miss an entire NFP release and the 30 minutes of volatile price action that follows. A 99.95% SLA halves that to approximately 22 minutes per month. A 99.99% SLA, the standard claimed by premium forex VPS providers, permits 52.6 minutes per year or 4.38 minutes per month. A 99.999% SLA allows just 5 minutes and 15 seconds per year, a level that requires redundant hardware and automatic failover that most single-VPS deployments cannot achieve.

The critical caveat: SLA credits compensate hosting cost, not trading losses. A provider that breaches its 99.99% guarantee refunds a percentage of the monthly VPS fee. If a 1-hour outage during an FOMC announcement costs a trader $500 in missed trades or unmanaged positions, the SLA credit covers perhaps $2 of the $30 monthly VPS bill. The SLA is a service commitment, not insurance.

Home PC availability compounds multiple failure points. Residential ISP uptime averages 99 to 99.5%. The PC itself (hardware, OS stability, power supply) runs at roughly 97 to 99%. Municipal power availability varies but 99 to 99.5% is typical for areas without backup power. These multiply: 99% PC uptime multiplied by 99.5% ISP multiplied by 99.5% power equals approximately 98.0%, translating to 175 hours of downtime per year. A worse-case scenario (97% PC, 99% ISP, 99% power) produces 95.1%, or roughly 430 hours per year. Windows forced update restarts, sleep mode activation, and hardware failures all contribute to the lower end of this range.

What breaks when the connection drops is specific and documented in official MetaTrader documentation. Trailing stops are client-side only. The official MT4 Help states: “Trailing Stop is always attached to an open position and works in client terminal, not at the server.” When the terminal disconnects, the trailing stop freezes. The last stop loss level set before disconnection remains active on the broker’s server, but it will not trail further until the terminal reconnects. Server-side orders survive: stop losses, take profits, and all pending order types (buy limit, sell limit, buy stop, sell stop) are stored on the broker’s server and execute regardless of terminal status. EA logic ceases entirely. All calculations, indicator updates, and new order placement stop immediately on disconnection. Open positions without SL or TP cannot be modified until the connection is restored.

One redundancy warning deserves specific mention. ForexVPS.net and FXVM are the same parent company (ThinkHuge Ltd) and experienced a simultaneous 24-hour outage in August 2025. A trader using both as “primary and backup” had no backup at all. A genuine backup VPS must use a provider with a different parent company and ideally a different data center operator.

Broker connectivity: execution models and what they mean for latency

The broker’s execution model determines whether VPS latency improvements translate into better fills or merely faster confirmation of the same outcome. A trader who spends $50 per month on a colocated VPS should understand whether their broker’s architecture actually benefits from that proximity.

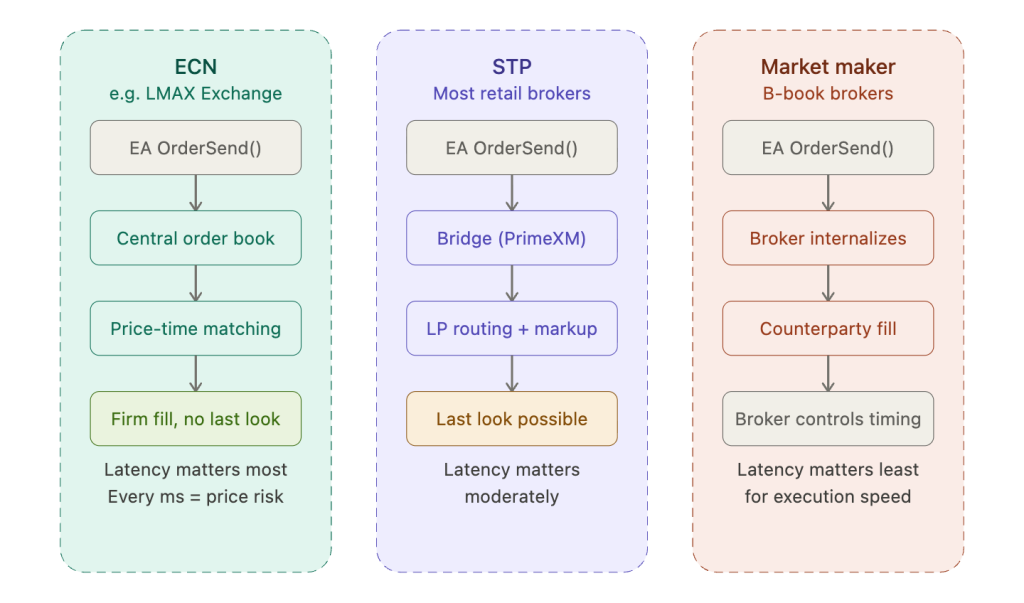

ECN execution routes orders to a central limit order book where they are matched against other participants’ orders with price-time priority. LMAX Exchange is the retail benchmark for this model: no dealing desk, no broker intervention, firm liquidity with no last look. Orders compete directly with other participants, including institutional flow and HFT firms. Latency matters most in this model because the price available at the moment the order arrives may differ from the price available 50ms later. Every millisecond of execution delay increases the probability that the intended price has moved. LMAX publishes internal exchange latency of under 50 microseconds and average trade latency including network of under 3ms. For ECN execution, the VPS investment pays for itself most directly.

STP (Straight Through Processing) is the model most retail “ECN” brokers actually operate. Orders are routed automatically to liquidity providers through bridge technology. The broker adds a markup or charges a commission but does not act as counterparty. Execution depends on LP response time and the efficiency of the bridge stack. PrimeXM, oneZero, Gold-i, and Takeprofit Tech are the major bridge providers. PrimeXM’s XCore platform explicitly supports “A-book, B-book and custom execution models” with real-time switching based on client profitability, trade size, and instrument. This hybrid capability means the execution model a trader experiences may change without notification. A well-built STP stack forwards orders to the LP matching engine in under 100 microseconds. A poorly built one introduces chronic slippage that no amount of VPS optimization can fix.

Market maker execution means the broker internalizes the order flow and acts as counterparty. The broker can execute instantly or introduce delay. Historically, MT4’s “virtual dealer plugin” allowed brokers to artificially add processing time to orders. VPS latency matters less for raw execution speed in this model because the broker controls the fill timing. It still matters for price accuracy (the price your EA sees should match the price it trades at) and for trailing stop updates, which require continuous client-side connectivity to adjust the stop loss level as price moves.

Last look is a mechanism where the liquidity provider retains the option to accept or reject a trade within an evaluation window measured in milliseconds. This adds processing time beyond what the network and bridge contribute. If the LP rejects the order, it must be re-routed to the next-best LP, adding further delay. Barclays discloses that its last look applies symmetrically, with settings varying by client, connection, and trading pattern. Academic research from Oxford (Cartea and Jaimungal) models last look as an option contract held by the LP. The NBIM (Norway’s sovereign wealth fund) acknowledges “intrinsic conflicts related to asymmetry in optionality.” LMAX Exchange explicitly operates with no last look, though the tradeoff is that LPs may offer less liquidity or wider spreads on a firm-quote venue. For VPS planning, last look means that a portion of the execution delay is structurally embedded and cannot be reduced through infrastructure improvement.

The ForexVPS.net latency experiment provides the only published attempt to quantify the financial impact of VPS location on execution quality. Over 120 trades, a London VPS (1ms ping to broker) showed +0.20 pips cumulative slippage while a New York VPS (75ms ping) showed -1.50 pips, a 1.70 pip difference attributable to latency. This experiment was conducted and published by a VPS provider with commercial interest in demonstrating that latency matters. It has not been independently replicated. The directional finding (lower latency correlates with less adverse slippage) is consistent with market microstructure theory and the Moallemi academic model, but the specific 1.70 pip figure should not be treated as a universal benchmark.

The distinction between requotes and slippage matters for infrastructure planning. Requotes occur when the broker rejects a trade at the requested price and offers an alternative. They are a broker-side behavior that infrastructure improvement cannot address. Slippage occurs when the order fills at a different price than requested. Slippage has an infrastructure-reducible component: it represents price movement during the execution window. Reducing that window through lower latency reduces the probability and magnitude of slippage but cannot eliminate it because market movement is continuous and liquidity gaps exist independently of execution speed.

Security, monitoring, and operational discipline

A trading VPS is a Windows server exposed to the internet with RDP access, running software that connects to financial accounts and potentially stores API keys for external services. The attack surface is larger than most traders realize, and the operational discipline required to maintain it is ongoing rather than one-time.

RDP is the primary attack vector. Sophos research found that RDP was exploited in 90% of cyberattacks targeting Windows servers. The default TCP port 3389 is the first target for automated scanners that continuously probe every public IP address. Changing the RDP port to a custom high-numbered value between 40000 and 65000 eliminates over 95% of automated attacks because the scanners move on to the next IP rather than probing non-standard ports. The registry path is HKLM\SYSTEM\CurrentControlSet\Control\Terminal Server\WinStations\RDP-Tcp, where the PortNumber value is changed. Beyond the port change, restrict inbound connections by IP in Windows Firewall (allow only the trader’s static home IP or VPN), enable Network Level Authentication (which forces authentication before a session is created), configure account lockout after 10 failed attempts, and block ports 445 (SMB) and 139 (NetBIOS) which serve no purpose on a trading VPS.

Monitoring a trading VPS requires three layers. UptimeRobot (free tier: 50 monitors at 5-minute intervals) handles VPS-level uptime by pinging the VPS IP or checking the custom RDP port. If the VPS goes down, the trader knows within 5 minutes via email, Telegram, or SMS. Myfxbook connects to MetaTrader via investor password and provides trade-level monitoring: growth charts, drawdown, risk exposure, and MAE/MFE analysis, updating every 5 minutes. For EA health specifically, MetaTrader’s built-in push notifications (configured in Tools, then Options, then Notifications with the MetaQuotes ID from the mobile app) alert the trader when the EA detects connection loss or error conditions. FX Blue’s suite adds capabilities that Myfxbook does not: an Account Monitor that notifies if the server goes down, an MT4 Auto-Restart EA that watches for connection issues and restarts the terminal, and Alert Forwarder that adds email and SMS to EAs lacking built-in notifications.

Maintenance discipline prevents the gradual degradation that catches traders weeks after initial setup. Weekly terminal restarts (scheduled via Task Scheduler: shutdown /r /f /t 60 every Saturday morning) clear accumulated memory growth that both MT4 and MT5 exhibit during extended operation, as documented across the scanner articles in this series. Log file cleanup on the same schedule prevents disk space exhaustion: delete .LOG files older than 30 to 60 days from the Logs and MQL5\Logs directories. Maintain a minimum of 10 to 20% free disk space. NTP clock synchronization using 4 or more independent time sources prevents clock drift that disrupts EA execution timing and API authentication timestamps. Windows Update management via Group Policy (gpedit.msc) should be configured to auto-download but schedule installation for Saturday at a specific time outside market hours, with “No auto-restart with logged on users” enabled to prevent forced reboots during trading.

For traders running AI-integrated EAs that store API keys (covered in detail in our AI trading tools guide), the most common vulnerability is hardcoded keys in EA source code or plaintext input parameters visible in configuration files on the VPS. Store keys in environment variables, restrict URL whitelist permissions to only required endpoints, and rotate keys periodically. The ForexVPS.net/FXVM simultaneous outage reinforces one final operational principle: a backup VPS must use a genuinely different provider with different parent company ownership and ideally a different data center operator.

The cost-latency curve: diminishing returns and tier planning

Every infrastructure improvement reduces latency, but the financial value of each millisecond removed follows a curve of diminishing returns. The Moallemi and Saglam model proves this mathematically: the marginal benefit of latency reduction increases as total latency approaches zero. Inverting that finding for practical VPS planning: the first large reduction (home PC to standard VPS) delivers the most value, and each subsequent improvement delivers proportionally less.

A home PC on broadband produces 200 to 500ms round-trip on MT4 and 100 to 300ms on MT5. A standard VPS in the same region as the broker ($20 to $40 per month) reduces this to 100 to 250ms on MT4 and 50 to 150ms on MT5. This first step eliminates 100 to 250ms of latency, adds 24/7 uptime (from 90 to 97% home availability to 99.9%+), and removes the trailing stop freeze risk during internet outages. For the majority of retail algo traders, this single upgrade delivers more execution improvement than every subsequent step combined.

A same-city or same-data-center VPS ($40 to $80 per month) brings latency to 5 to 20ms on the network leg. Combined with MT5’s 1 to 2ms platform processing, realistic round-trip reaches 30 to 80ms. The improvement over a standard regional VPS is 20 to 120ms. Meaningful for scalping strategies where positions are held for minutes and every pip of slippage compounds across hundreds of trades per month. Less impactful for swing trading on H4 or D1 timeframes where a 50ms difference does not affect the fill price on an order that will be open for hours or days.

A colocated VPS with cross-connect ($80 to $200 per month plus $100 to $300 for the cross-connect) achieves sub-1ms network latency. The improvement over a same-city VPS is perhaps 5 to 19ms on the network leg. Whether this justifies the cost depends entirely on trade frequency. For a trader executing 5 trades per day on H1 charts, the latency improvement is invisible in the P&L. For a trader executing 200 trades per day on M1 with a scalping EA, even 10ms of improvement compounds into measurably less slippage over a month.

Beyond colocation, the next step is not a better VPS. It is bypassing MetaTrader entirely via FIX API, which achieves 5 to 20ms full round-trip by eliminating the platform processing layer. This requires a broker that offers FIX connectivity (LMAX, some institutional-grade STP brokers), custom software development, and substantially more technical capability than MetaTrader EA deployment. It is a different infrastructure category, not a VPS upgrade.

The MetaQuotes built-in VPS ($12.80 to $15 per month) occupies a specific position on this curve. It offers exceptional latency (96% of broker servers reachable under 10ms) at the lowest cost in the market. The constraints are severe: no DLL support (breaking Python bridges, ZeroMQ, and ML-based EAs), no RDP access, a 3 GB RAM maximum, one trading account per subscription, and a 32-chart limit. For a single simple EA on a single account with no external integrations, it is difficult to beat on value. For anything more complex, the limitations force a full Windows VPS.

Hidden costs on third-party VPS providers add $5 to $25 per month beyond the headline price: Windows Server licensing ($5 to $15 if not included), backup services (some providers advertise “included” backups that are actually a paid add-on), and premium monitoring tiers. A $20 per month VPS can cost $40 per month after these additions.

When does the VPS pay for itself? On a $10,000 account making 50 trades per month on EUR/USD standard lots, 0.5 pips of average slippage improvement equals approximately $25 per month. At $15 to $30 per month for a standard VPS, the investment breaks even from slippage reduction alone, before accounting for the uptime value of preventing missed trades during the 263 to 876 hours of annual downtime that a home PC produces.

FAQ

Does my VPS need to be close to me or close to my broker?

Close to your broker. The VPS replaces your home PC as the execution point, so the latency that matters is VPS-to-broker, not you-to-VPS. You connect to the VPS via RDP for configuration and monitoring, and RDP tolerates 100 to 200ms of latency without noticeable impact on usability. A trader in Singapore whose broker servers are in Equinix LD4 (London) should provision a VPS in or near LD4, not in Singapore. The 160 to 180ms between Singapore and London would apply to every trade if the VPS were in Singapore. With the VPS in London, that latency applies only to the RDP session, which has no effect on execution speed.

Can I use AWS or DigitalOcean instead of a forex-specific VPS?

Technically yes. AWS EC2 and DigitalOcean droplets run Windows Server and can host MetaTrader. The practical considerations are cost and configuration. An AWS t3.medium (2 vCPU, 4 GB RAM) runs approximately $30 to $50 per month plus Windows Server licensing, comparable to a mid-tier forex VPS. The difference is setup and support: a forex-specific provider pre-installs Windows, may offer MetaTrader pre-configuration, provides broker latency data for server location selection, and understands trading-specific support tickets. AWS and DigitalOcean offer none of this. For a trader comfortable with Windows Server administration and willing to do their own latency testing, generic cloud providers work. For a trader who wants to provision and start trading within an hour, a forex-specific provider is worth the modest premium.

How do I find which data center my broker uses?

Start with the broker’s official website. IC Markets and FxPro publish facility names (NY4, LD4) explicitly. Most brokers do not. For the rest, open MetaTrader and note the server address in File, then Open Account. Use the command line to ping that address and record the IP. Enter the IP into ipinfo.io to identify the city and hosting provider. Run traceroute (tracert on Windows) to see the network path and identify the data center operator from hop names. If traceroute shows Equinix hostnames in the final hops, you have strong evidence. Contact broker support directly and ask which facility their trade servers are in. Check VPS provider broker latency databases (MassiveGRID publishes a table of broker locations). Cross-reference multiple sources because no single method is definitive.

Does MT5 execute faster than MT4 on the same VPS?

Yes, by approximately 48ms per order on internal platform processing alone (MT4 at roughly 50ms versus MT5 at 1 to 2ms). This is an architectural difference documented by MQL5 forum administrators, not a configuration issue that tuning can resolve. MT5 also eliminates the single trade context bottleneck (Error 146) that forces MT4 traders to run separate terminal instances for each EA that trades. For multi-EA deployments, MT5 reduces both latency per order and total RAM consumption by consolidating EAs into fewer terminal instances. The tradeoff is higher per-terminal memory baseline (250 to 350 MB versus 150 to 200 MB for MT4), which matters on constrained VPS tiers. Our MT4 vs MT5 VPS comparison covers the full platform decision in detail.

Is colocation worth it for a retail trader?

For most retail traders, no. A same-region VPS ($20 to $40 per month) eliminates the largest controllable latency component (home broadband) and provides 24/7 uptime. The improvement from same-region to colocated is typically 20 to 50ms on the network leg, which matters for M1 scalping strategies executing hundreds of trades per month but is invisible in the P&L of a swing trader on H4 or D1. Colocation becomes worth the cost when trade frequency is high enough that cumulative slippage reduction exceeds the additional VPS expense. A trader executing 200 trades per month might save 0.3 to 0.5 pips per trade from 20ms of latency reduction, producing $30 to $50 per month of measurable improvement on standard lots. A trader executing 10 trades per month will not recover the colocation premium from execution improvement alone.

References

- Bank for International Settlements. “Triennial Central Bank Survey of Foreign Exchange and Over-the-counter (OTC) Derivatives Markets in 2025.” FX turnover reached $9.6 trillion per day in April 2025, up 28% from $7.5 trillion in 2022. Spot FX: $3 trillion/day. USD on one side of 89.2% of trades. 52 jurisdictions, 1,100+ reporting banks. Most current available data; most competitor articles still reference 2022 figures.

- Moallemi, C.C. and Saglam, M. “The Cost of Latency in High-Frequency Trading.” Operations Research, Vol. 61, No. 5, 2013. Reducing latency from 500ms to 5ms reduces cost of immediacy from 100% to 5%. Marginal benefit increases as latency approaches zero. Peer-reviewed, foundational academic paper. Theoretical model, not empirical forex measurement.

- Hasbrouck, J. and Saar, G. “Low-Latency Trading.” Journal of Financial Markets, Vol. 16, 2013. Low-latency activity improves market quality: narrower spreads, reduced short-term volatility.

- BIS Working Paper No. 955. “Quantifying the HFT Arms Race.” Latency arbitrage costs estimated at $2.3 to $8.4 billion per year globally. Uses exchange message data.

- MetaQuotes Software Corp. MQL5 Forum. Administrator-confirmed MT4 internal processing latency of approximately 50ms. MT5 internal processing approximately 1 to 2ms. Multiple independent user confirmations across forum threads.

- MetaQuotes Software Corp. MQL5 Forum. MT4 30-second session timeout requiring re-authentication, adding 200 to 2,000ms. Originally documented by ForexFactory user “rooicol,” widely confirmed across MQL5 and ForexFactory communities.

- MetaQuotes Software Corp. Official MT4 Help documentation. Trailing stops: “Trailing Stop is always attached to an open position and works in client terminal, not at the server.” Server-side orders (SL, TP, pending) survive terminal disconnection.

- MQL5 Forum. William Roeder (32,000+ posts). News event execution: “can take minutes to do a trade because of the servers during news.” Forum measurements during volatile conditions: 3,000 to 6,000ms per trade. One extreme case: 150,063ms for a single MT5 OrderSend.

- LMAX Exchange. Official press materials and e-Forex Magazine coverage. Internal exchange latency: under 50 microseconds. Average trade latency including network: under 3ms. Matching engines in LD4, NY4, TY3, SG1. Capacity: 40,000 orders per second. No last look, firm liquidity on central limit order book.

- IC Markets. Official website. Confirms colocation “in the Equinix NY4 Data Centre.” UK operations reference LD5. Primary source, highest confidence level for broker location data.

- FXCG/Capstone Markets. Official website. Confirms NY4 and LD5 presence. Primary source.

- FxPro. FX News Group press release. “Dedicated physical cross-connect within Equinix LD4.” Primary source.

- Colo-X/MassiveGRID. Independent data center broker. LMAX Exchange confirmed in LD4 since Q4 2012. Cross-facility latency data: LD4 to NY4 65 to 75ms, LD4 to Frankfurt 7 to 12ms, LD4 to Amsterdam 5 to 8ms, LD4 to TY3 200 to 220ms. Commercially interested source.

- Beeks Group (LSE: BKS). NY5 cross-connect list includes Deutsche Bank, Barclays, Goldman Sachs, UBS, HSBC, Morgan Stanley, Interactive Brokers, LMAX. Publicly listed company. Bronze plan: £31/month. Forex Peace Army user reviews: 2.14/5 (12 reviews).

- NYCServers. Broker ping measurements from NY4-area infrastructure: IC Markets 1.03ms, Pepperstone 1.03ms, OANDA 0.98ms, FXCM 1.02ms. Single commercially interested source, not independently verified.

- PrimeXM. Official website. Claims “sub-millisecond connectivity” when colocated in LD4, NY4, TY3. XCore platform supports A-book, B-book, and custom execution models with real-time switching. Commercially interested source; no independently verified latency benchmarks published.

- oneZero. Official website. C++ architecture, dedicated hosted instances, colocated NY4, LD4, TY3. Commercially interested source.

- ForexVPS.net. Latency experiment: 120 trades, London VPS (1ms) showed +0.20 pips cumulative slippage, NYC VPS (75ms) showed -1.50 pips. 1.70 pip difference. VPS provider study, not independently replicated. ForexVPS.net and FXVM share parent company ThinkHuge Ltd; simultaneous 24-hour outage in August 2025.

- Barclays. barx.com disclosure. Last look applies symmetrically, settings vary by client, connection, and trading pattern.

- Cartea, A. and Jaimungal, S. University of Oxford. Models last look as option contract held by the liquidity provider. NBIM (Norges Bank Investment Management) acknowledges “intrinsic conflicts related to asymmetry in optionality.”

- Sophos. Research on RDP exploitation: 90% of cyberattacks targeting Windows servers used RDP as the attack vector. Cited via TradingFXVPS; original Sophos report should be verified independently.

- European Securities and Markets Authority. MiFID II Article 17. Requires effective systems and risk controls for algorithmic trading. HFAT defined as infrastructure minimizing latency via colocation, proximity hosting, or high-speed direct electronic access. Kill-switch requirements, algorithm testing before deployment.

- FINRA. Rule 3110 (supervision of algorithmic strategies), Rule 6820 (business clocks within 50ms of NIST standards). SEC Regulation NMS (best execution obligations).

- FXVPS.biz. Market Watch cleanup yielding 20 to 40% CPU reduction. Single commercially interested source, not independently verified. Cross-article consistent flagging.

Editorial Note

This article maps the infrastructure stack for retail forex algorithmic trading: execution chain, data center geography, VPS architecture, uptime, broker connectivity, security, and cost. It does not constitute financial advice, trading strategy guidance, or a recommendation of any specific broker, VPS provider, or data center facility. No endorsement of named brokers or infrastructure providers is intended. They are included because specific, verifiable examples build a more useful reference than generic descriptions.

Latency figures throughout this article are reference ranges, not guaranteed specifications. Actual execution times vary by broker infrastructure, liquidity conditions, time of day, market volatility, platform version, and VPS provider quality. The MT4 50ms and MT5 1 to 2ms internal processing figures come from MQL5 forum administrators, not official MetaQuotes documentation. Bridge latency figures could not be independently verified from public sources; bridge providers universally avoid publishing specific benchmarks.

Data center presence confirmations range from primary sources (broker official websites) to medium-confidence sources (VPS provider tables). Confidence levels are noted inline. VPS provider latency measurements (NYCServers, MassiveGRID, ForexVPS.net) are commercially interested sources with incentive to demonstrate that latency and location matter.

The BIS and academic citations (Moallemi, Hasbrouck) provide the strongest factual foundation. Their findings are from institutional and exchange-traded contexts and may not translate directly to retail forex execution on MetaTrader platforms.